Credit Card Approval Guide: How to Get Approved Easily in 2026

This 2026 guide shares proven, up-to-date strategies to get approved for a credit card fast—even with bad credit or no credit history. Learn application steps, issuer hacks, and how to avoid common denials.

Getting approved for a credit card in 2026 doesn’t have to be stressful. Whether you’re building credit for the first time, rebuilding after missteps, or just want a better approval rate, the rules and hacks have shifted slightly this year. This guide cuts through the noise with 2026-specific tips, step-by-step application advice, and insider tricks to boost your odds—so you can get approved easily and start using your card sooner.

Why 2026 Is Different for Credit Card Approvals

Credit card issuers tightened standards slightly in late 2025, but 2026 has brought more flexible options for bad credit, thin credit files, and first-time applicants. Key shifts include:

- More unsecured credit cards for low credit scores (550–650 FICO).

- Relaxed income verification for part-time and gig workers.

- New pre-approval tools that don’t hurt your credit score.

- Higher approval rates for applicants with 3+ months of on-time bill payments.

Even with these changes, denials still happen—usually from mismatched card choices, too many applications, or hidden credit report errors. The good news? Most are avoidable with the right prep.

Step 1: Check & Fix Your Credit Report (Critical for 2026 Approval)

Before applying, pull your 2026 credit report (Experian, Equifax, TransUnion) and fix errors—this alone can boost your score by 50+ points and prevent instant denials.

- What to look for: Late payments you didn’t make, incorrect balances, or accounts you don’t recognize.

- How to fix: File a dispute online with the credit bureau—most errors are resolved in 30 days.

- Pro Tip for 2026: Free tools like Credit Karma or Capital One Credit Tracker let you check your FICO 8 score (the one issuers use) for free—avoid VantageScore, which can differ by 50+ points.

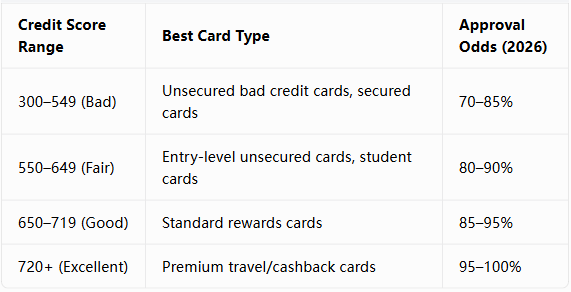

Step 2: Match Your Card to Your Credit Score (Avoid Instant Denial)

The #1 reason for rejection in 2026? Applying for premium cards (700+ FICO) when your score is fair or poor. Use this quick 2026 cheat sheet:

2026 Top Picks for Easy Approval:

- Bad Credit: Capital One QuicksilverOne (unsecured, 550+ score).

- First-Time Applicants: Discover it® Student Cash Back (no credit history required).

- No Annual Fee: Chase Freedom Flex (fair credit welcome).

Step 3: Master the 2026 Application Timing & Spacing Rules

Issuers penalize “credit shopping” more heavily in 2026. Follow these timing rules to keep your application clean:

- Same Issuer: Wait 90+ days between applications (e.g., two Capital One cards).

- Different Issuers: Wait 30+ days (e.g., Chase then Amex).

- After Denial: Wait 3–6 months before reapplying—too soon signals desperation.

- Best Time to Apply: After a credit score increase, when your income rises, or when old inquiries fall off (2 years).

Critical 2026 Rule: No more than 2 applications in 3 months. More than that = automatic denial from most major issuers.

Step 4: How to Apply for a Credit Card in 2026 (Step-by-Step for Fast Approval)

The 2026 application process is fully online and faster than ever—follow these steps to avoid mistakes:

Step 4.1: Get Pre-Approved First (No Credit Hit)

Before applying, use 2026’s free pre-approval tools to see which cards you qualify for—this doesn’t affect your credit score.

- Where to check: Capital One, Discover, and Credit Karma offer pre-qual checks for multiple issuers.

- Why it works: Pre-approval uses a “soft inquiry,” so your score stays intact. Only apply for cards you’re pre-approved for.

Step 4.2: Prepare Your 2026 Application Info (100% Accurate)

Issuers verify all details in 2026—even small lies = instant denial. Have these ready:

- Full legal name, address, and SSN.

- Employment status (full-time, part-time, gig, or retired).

- Monthly income (include side hustles, alimony, or passive income—gig workers get extra flexibility in 2026).

- Monthly rent/mortgage payment.

Step 4.3: Submit Your Application & Get Instant Decision

Fill out the online form, review terms, and submit. Most 2026 applications give an instant decision (approved, denied, or pending review).

- If approved: Note your credit limit, APR, and fees—activate your card online immediately.

- If pending: Wait 3–7 days for manual review—avoid applying for other cards in the meantime.

Step 5: 2026 Hacks to Boost Approval Odds (Even with Bad Credit)

These insider tricks work in 2026 for bad credit, first-time applicants, and thin credit files:

Hack 1: Use Unsecured Credit Cards for Bad Credit

Secured cards require a deposit, but 2026’s best unsecured bad credit cards (e.g., Capital One QuicksilverOne, Milestone Gold Mastercard) approve applicants with 550+ scores—no deposit needed. They report to credit bureaus, so you build credit while using the card.

Hack 2: Lower Your Credit Utilization Before Applying

Credit utilization (how much of your available credit you use) makes up 30% of your FICO score. In 2026, keep it below 30% (e.g., $300 balance on a $1,000 limit). Pay down high balances 1–2 months before applying—this can raise your score by 20+ points.

Hack 3: Add a Co-Signer or Become an Authorized User

If you have no credit or bad credit, ask a trusted friend/family member with good credit to co-sign your application—this doubles your approval odds in 2026. Alternatively, become an authorized user on their card—their positive payment history boosts your score.

Hack 4: Call the Reconsideration Line If Denied

A denial isn’t final in 2026. Every major issuer has a reconsideration line—call to explain your situation (e.g., “I have a long history with your bank” or “I can lower my credit limit to get approved”). This works 30–40% of the time for applicants with minor issues.

2026 Reconsideration Numbers:

- Chase: 1-888-270-2127

- American Express: 1-800-567-1083

- Capital One: 1-800-625-6242

Step 6: Avoid These 2026 Credit Card Application Mistakes

Even small missteps can lead to denial—steer clear of these:

- Applying for too many cards at once: 3+ applications in 3 months = automatic denial.

- Ignoring annual fees: Some easy-approval cards have high fees—read terms carefully.

- Lying about income: Issuers verify income in 2026—falsification = permanent ban from the issuer.

- Closing old cards: This shortens your credit history and lowers your score—keep old accounts open.

Final Thoughts: Get Approved Easily in 2026

Getting approved for a credit card in 2026 is simple when you follow the rules: check your credit, match your card to your score, time applications wisely, and use pre-approval tools. Even with bad credit or no credit history, unsecured cards and issuer hacks make approval achievable.

Once approved, use your card responsibly—pay bills on time, keep utilization low—and you’ll build great credit. By 2027, you’ll qualify for premium cards with better rewards and lower rates.